|

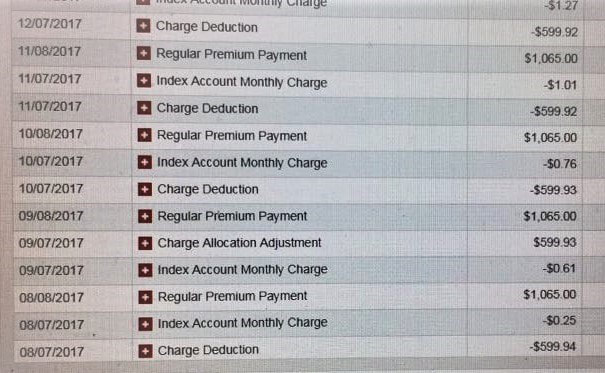

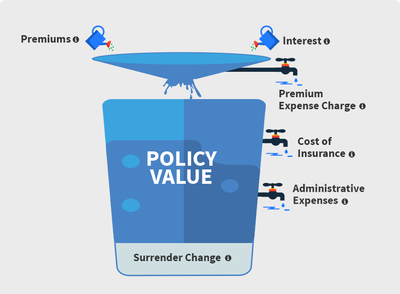

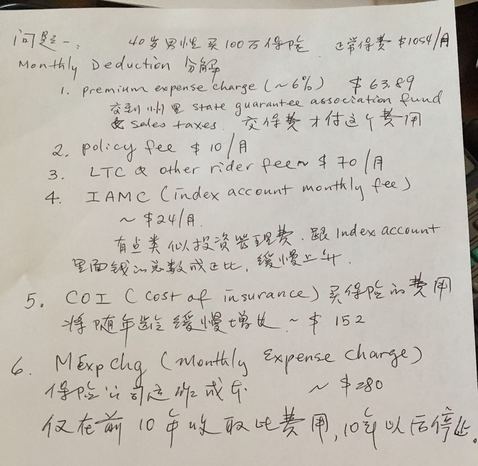

Explaining the costs and fees to clients  My client got a $1 million FFIUL policy. The policy was approved. I helped her to set up an online account on the TPLIC website. Next month she sent me a message with following screen shot of her account: She asked about the -$599.92 monthly charge deduction and said that this policy is too expensive. How should you explain to her about it? Let's first figure out where premium goes after the insurance company receives a premium: Now about the charges and fees: Premium Expense Charge The following charge is applied to all premium payments, including 1035 Exchanges, prior to the payment being allocated to the Account Options. (no premium, no charge) Current: Year 1: 4% (8% in Puerto Rico) Years 2-10: 6% (10% in Puerto Rico) Years 11+: 2% (6% in Puerto Rico) Guaranteed: 6% in all years (12% in Puerto Rico) Index Account Monthly Charge The Index Account Monthly Charge is 0.06% (0.72% annually) of the Index Account Value (current and guaranteed). This charge is taken on the Monthly Policy Date through age 120, from the highest numbered Segment first. Monthly Deductions Monthly Deductions will be taken from the Basic Interest Account and the Index Accounts in proportion to the values of those accounts on the Monthly Policy Date. The Monthly Policy Date is the same day in each month as the policy date. Monthly Deductions will be taken from the highest numbered Segment first and then from the next highest numbered Segment. On each Monthly Policy Date, a deduction will be made from the Policy Value equal to the sum of the following fees and charges: Monthly Policy Fee: Current: $10 Guaranteed Maximum: $12 Monthly Cost of Insurance charge: (COI) The current monthly Cost of Insurance (COI) charge depends on several factors such as the Face Amount, risk class, age, gender, and duration, as well as the difference between the Policy Value and death benefit. The COI charges will vary each month. Please see the policy for details. Monthly Expense Charge: The Monthly Expense Charge is shown in the policy data pages. This charge applies for the first ten policy years and ten years from the date of any requested increase in Face Amount. On a guaranteed basis, this charge applies for ten years from issue or increase date for ages 0-60 and through age 120 for issue ages 61-85 for states other than Florida. In Florida, the guaranteed charge applies through age 120 for all issue and increase ages. This charge varies by issue age, sex, band and tobacco use. This charge is also applied to any Additional Insured Rider for eight years from rider issue date and eight years from the date of any increase in rider Face Amount. Any change in the Monthly Expense Charge will be applied uniformly to all policies with the same Face Amount, age, sex and class of risk that have been in effect for the same length of time. Rider charges, if any. Surrender charge: No charge if no surrender.   My client's -$599 monthly deduction: 1. Premium expenses (similar to sales tax and fee to state guarantee association): $63.99/month Notes: 1) This only applies to new premium. It is not a compounding charge. 2) When you stop paying the premium, you don't have this charge. 2. Policy fee: $10/month 3. LTC and other rider charge: $70/month 4. IAMC (index account monthly fee): $24/month 5. COI: cost of insurance. $ 152/month Note: This one will increase when the insured is older, but will decrease with the cash value accumulation. That's why we encourage the client to overpay during the early years. 6. Monthly Expense Charge (MExChg): $280/month. Note: This charge will go away after 10 years. Also you can remind the client that yes, the IUL is expensive in early years, but the charges won't grow that much even when they are old. (See the illustration above). On the other hand, charges in a 401K or mutual fund account will grow a lot when they have more money in it.  |

RSS Feed

RSS Feed

|

|